🕜 Quick Answer

What is Video KYC in India?

Video KYC (V-CIP) is a live video-based identity verification method under RBI KYC Master Direction Para 19. It is the only digital eKYC method treated as face-to-face equivalent —removing the ₹1 lakh/year transaction cap. Required for banks, NBFCs, and fintechs onboarding high-value customers. eKYCNow delivers it at ₹18/session with deepfake-proof liveness.

What Is Video KYC (V-CIP) in India?

Video KYC — officially called Video Customer Identification Process (V-CIP) — is a real-time video-based identity verification method introduced by RBI in January 2020 (Para 19 of the KYC MasterDirection) and significantly strengthened by the August 2025 amendment.

Unlike Aadhaar OTP eKYC, which RBI classifies as non-face-to-face (carrying a ₹1 lakh/year transactioncap), V-CIP is the only digital KYC method granted face-to-face equivalent status. This makes itessential for any regulated entity offering high-value financial products — personal loans, wealthmanagement, full-feature current accounts, insurance policies above ₹1L.

RBI Para 19 — The Law

RBI KYC Master Direction Para 19 (January 2020, amended August 2025): "REs [Regulated Entities] may use Video based Customer Identification Process (V-CIP) as a consent-based alternate method of establishing the customer's identity for CIP. V-CIP shall be treated as face-to-face customer identification process for the purpose of this Direction." Full regulatory guide: RBI KYC Compliance India

RBI Para 19 Requirements Checklist

For a Video KYC session to be Para 19-compliant, all of the following must be met:

| Requirement |

What it means |

eKYCNow handles? |

| Live video connection |

Real-time, unrecorded-first session between customer and trained official |

✓ Automated + human-in-loop options |

| Face match to OVD |

Customer's live face compared to Aadhaar/PAN photo using AI |

✓ 99.2% accuracy |

| PAN verification |

PAN number verified against NSDL during session |

✓ Real-time NSDL query |

| Geo-tagging |

Customer's location must be in India and captured |

✓ Auto geo-tag with consent |

| End-to-end encryption |

Session must be encrypted throughout |

✓ TLS 1.3 + AES-256 |

| 5-year encrypted storage |

Full session recording stored for audit |

✓ Encrypted cloud storage |

| Deepfake prevention |

Added August 2025: must detect AI-generated faces and video replays |

✓ 99.4% deepfake detection |

| Customer consent |

Explicit consent for video recording must be obtained |

✓ Consent screen built-in |

| Trained official |

RE employee must be trained and certified for V-CIP |

✓ eKYCNow provides training module |

OTP eKYC vs Video KYC — Which Do You Need?

⚡

Rule of thumb: If your product involves transactions above ₹1 lakh/year or requires standard CDD (not EDD), you need Video KYC. OTP eKYC alone is not sufficient.

| Factor |

OTP eKYC / Offline Aadhaar |

Video KYC V-CIP |

| RBI classification |

Non-face-to-face |

Face-to-face equivalent |

| Transaction cap |

₹1 lakh/year |

No cap |

| Due diligence tier |

EDD (Enhanced) |

Standard CDD |

| Suitable for loans? |

Only below ₹1L |

✓ All loan sizes |

| Deepfake risk |

Medium (OTP can be shared) |

Very low (live liveness check) |

| Time |

<1 second |

4–6 minutes |

| eKYCNow price |

₹10/check |

₹18/session |

How eKYCNow Video KYC Works

| Factor |

OTP eKYC / Offline Aadhaar |

Video KYC V-CIP |

| RBI classification |

Non-face-to-face |

Face-to-face equivalent |

| Transaction cap |

₹1 lakh/year |

No cap |

| Due diligence tier |

EDD (Enhanced) |

Standard CDD |

| Suitable for loans? |

Only below ₹1L |

✓ All loan sizes |

| Deepfake risk |

Medium (OTP can be shared) |

Very low (live liveness check) |

| Time |

<1 second |

4–6 minutes |

| eKYCNow price |

₹10/check |

₹18/session |

01

Send secure link

Customer receives a one-time

secure V-CIP link via SMS or

WhatsApp. No app download

needed.

02

Customer joins

Browser-based session opens.

Consent screen captured.

Geo-tag + device check auto-

runs.

03

Liveness check

Passive multi-frame liveness +

active challenge (blink/turn).

Deepfake detection runs in

parallel.

04

Document capture

Customer holds Aadhaar/PAN

to camera. AI reads, validates,

and face-matches in real-time.

05

PAN verification

PAN number queried against

NSDL live. Name + DOB cross-

checked against document.

06

Result + CKYC upload

Session result returned via

webhook. CKYC record auto-

uploaded to CERSAI within 3

days.

Deepfake Prevention — August 2025 Requirement

The August 2025 RBI amendment formally added presentation attack detection and deepfakeprevention as explicit V-CIP requirements. This is a significant tightening — basic face-movementprompts are no longer sufficient.

eKYCNow's deepfake protection stack:

- Passive liveness analysis: Multi-frame texture analysis detects printed photos, video replays, andsilicone masks without requiring customer action.

- Active challenge-response: Random challenges (gaze direction, expression) verify the customer isphysically present.

- AI deepfake classifier: Frame-by-frame GAN detection trained on Indian deepfake datasets. 99.4%accuracy.

- Velocity fraud signals: Cross-session signals detect coordinated fraud attempts using the sameface across multiple sessions.

⚠️ Compliance risk: If your Video KYC provider doesn't have explicit deepfake detection as per the August 2025

amendment, your V-CIP sessions may not be Para 19-compliant.

| Factor |

OTP eKYC / Offline Aadhaar |

Video KYC V-CIP |

| RBI classification |

Non-face-to-face |

Face-to-face equivalent |

| Transaction cap |

₹1 lakh/year |

No cap |

| Due diligence tier |

EDD (Enhanced) |

Standard CDD |

| Suitable for loans? |

Only below ₹1L |

✓ All loan sizes |

| Deepfake risk |

Medium (OTP can be shared) |

Very low (live liveness check) |

| Time |

<1 second |

4–6 minutes |

| eKYCNow price |

₹10/check |

₹18/session |

Video KYC by Industry in India

🏦

Banks & Scheduled Banks

Full-service account opening. V-CIP removes all transaction

restrictions.

🏢

NBFCs

Loan origination above ₹1L. V-

CIP mandatory for standard CDD classification.

📊

Wealth Management

Investment account opening.

SEBI requires KYC equivalent to bank standards.

🛡️

Insurance (IRDAI)

Policy issuance above ₹1L. V-CIP accepted by IRDAI for remote onboarding.

₿

Crypto Exchanges

FIU-IND PMLA compliance. V-CIP for premium tier user

onboarding.

📱

Lending Fintechs

Personal loan, BNPL, credit line origination. Single V-CIP session covers all products.

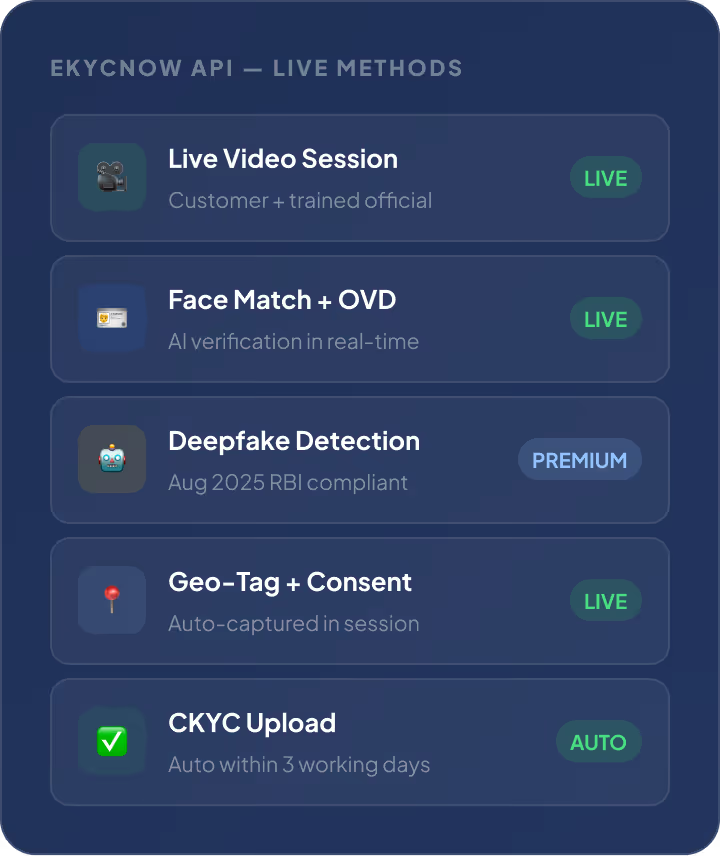

Video KYC API Integration

eKYCNow Video KYC integrates via a single REST API. Send the customer's mobile number, receive asession URL, and get a result webhook when complete:

⚙️

POST /v1/video-kyc/initiate → returns session_url + session_id. Send session_url to customer via SMS/WhatsApp. Receive result at your webhook: status (pass/fail/manual_review), face_match_score, liveness_score, deepfake_score, pan_verified, geo_lat/long. Full docs: API India docs →

| Factor |

OTP eKYC / Offline Aadhaar |

Video KYC V-CIP |

| RBI classification |

Non-face-to-face |

Face-to-face equivalent |

| Transaction cap |

₹1 lakh/year |

No cap |

| Due diligence tier |

EDD (Enhanced) |

Standard CDD |

| Suitable for loans? |

Only below ₹1L |

✓ All loan sizes |

| Deepfake risk |

Medium (OTP can be shared) |

Very low (live liveness check) |

| Time |

<1 second |

4–6 minutes |

| eKYCNow price |

₹10/check |

₹18/session |

Video KYC Pricing in India

| Factor |

OTP eKYC / Offline Aadhaar |

Video KYC V-CIP |

| RBI classification |

Non-face-to-face |

Face-to-face equivalent |

| Transaction cap |

₹1 lakh/year |

No cap |

| Due diligence tier |

EDD (Enhanced) |

Standard CDD |

| Suitable for loans? |

Only below ₹1L |

✓ All loan sizes |

| Deepfake risk |

Medium (OTP can be shared) |

Very low (live liveness check) |

| Time |

<1 second |

4–6 minutes |

| eKYCNow price |

₹10/check |

₹18/session |

Full India pricing breakdown →